Examining the data on a paycheck stub matters because the stub is the one document that answers, on a single page, whether an applicant earns enough, whether the income is real, and whether it is stable — and a glance at the headline salary answers none of those. A reviewer who reads only the big number approves bad files and rejects good ones; a reviewer who reads the data underneath catches both. The ten data points worth examining, in the order they decide a rental file, are:

- Gross pay — does the income clear the 3× rent rule?

- Pay frequency — is the income annualizing correctly, or does a big semi-monthly figure hide a modest annual one?

- Year-to-date (YTD) gross — is the income stable and continuous, or does it fail to annualize to the salary claimed?

- Net pay — does the take-home actually land in the bank account?

- Tax withholding — are federal, Social Security, and Medicare lines present (proof of real W-2 employment)?

- Employer identity — is there a name, address, and phone a reviewer can call?

- Pay-period dates — is the stub recent and the employment continuous?

- Deductions — do garnishments or support orders quietly shrink real disposable income?

- Reconciliation math — does gross minus deductions actually equal net?

- Cross-document consistency — do the stub, bank statement, ID, and application agree?

The wage data on a stub is the same data the federal Fair Labor Standards Act requires every employer to keep on file, which is what makes a genuine stub internally consistent and a fabricated one detectable — fake stubs almost always break on the math before they break on anything else. Examining the data is also what keeps a screening decision defensible: a tenant-screening report is a consumer report under the Fair Credit Reporting Act, so a denial has to rest on a real, documented reason, not a hunch about a number.

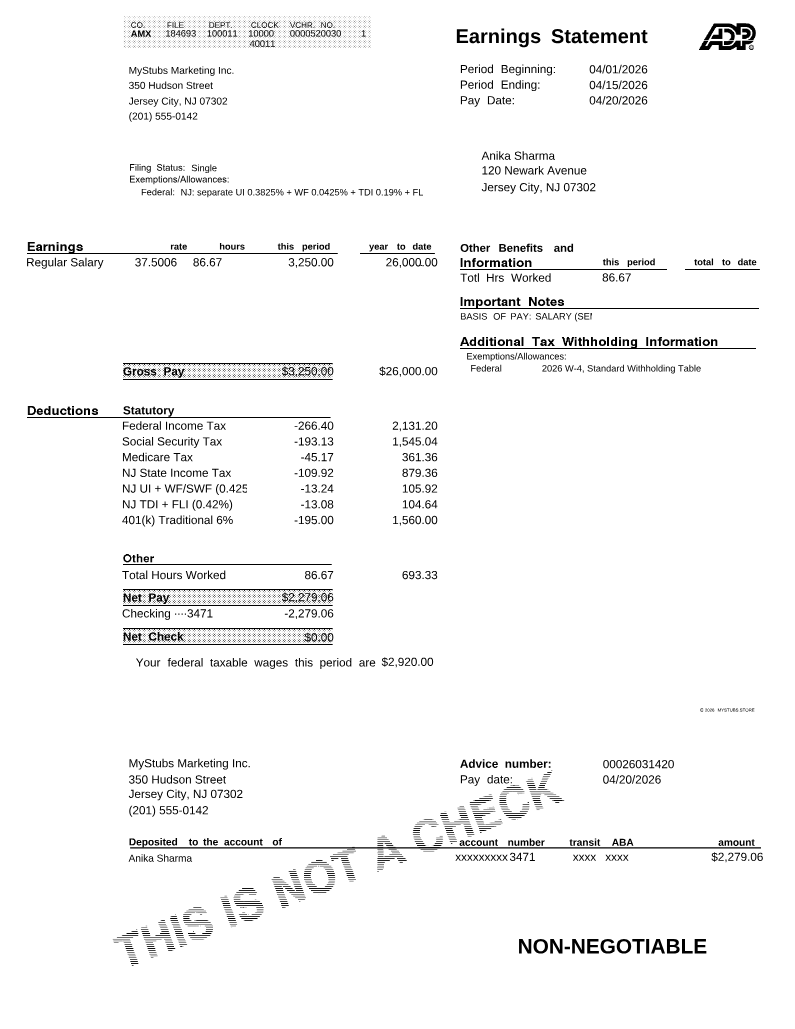

Throughout this guide the worked example is Renée Alvarez, a property manager screening Caleb Monroe for a $2,100/month unit in Columbus, Ohio. Caleb's stub claims $80,000/year, paid biweekly — a file that examination confirms as real, and a template for what examination would have caught if it were not. If you want to reproduce the gross-to-net math a reviewer checks, the MyStubs paycheck calculator runs the period reconciliation for any state.

Paystub Generator

See what a clean, reconciling stub looks like

The MyStubs paystub generator renders pay stubs where gross, taxes, YTD, and net all tie out — the same internal math a leasing reviewer examines. Use it to document real wages cleanly, or to learn what a reconciling stub is supposed to look like before you examine someone else's.

Build a Reconciling StubThe Cost of Not Examining the Data

A reviewer who skips the data examination makes two expensive errors. The first is the false positive: approving a fabricated or insufficient stub, then chasing rent for a year. The second is the false negative: rejecting a fully qualified applicant over a number that looked odd but was actually fine — a borderline ratio, a mid-year start, a state with four payroll deductions. Both errors are avoidable, and both come from reading the headline instead of the data.

For the renter, the same examination is a pre-flight check. Examining your own stub before you apply catches the mismatches a reviewer would catch — a nickname instead of your legal name, a net that does not match your deposits, a YTD that does not annualize because you started in March — while you still have time to explain or correct them. It also tells you whether your stub alone is enough proof of income for the apartment or whether you need to add documents. The examination is identical; only the seat changes.

Paystub Generator

Create your paystub in minutes

Build a professional paystub with built-in 2026 tax math, all 50 states, and instant PDF download.

Create Your PaystubTen Data Points and What Examining Each Reveals

The annotated figure below marks the data points a reviewer examines, in roughly the order they decide a file. Hover or focus any numbered chip for the data point it labels.

Hover or focus any numbered chip for the data point it labels.

The numbered legend, with what examining each data point reveals and Caleb's entry:

- Gross pay. — the pre-tax figure the 3× rule runs on. Reveals whether income supports the rent. Caleb: $3,076.92/period → $6,666.67/month, above the $6,300 needed for a $2,100 unit (3.17×).

- Pay frequency. — weekly, biweekly, semi-monthly, monthly. Reveals the true annual figure; a $3,000 semi-monthly stub is $72,000/year, but the same $3,000 weekly is $156,000 — examining frequency prevents both over- and under-counting. Caleb: biweekly, 26 periods.

- Year-to-date gross. — the running annual total. Reveals stability and continuity; it should annualize to the salary claimed. Caleb at period 14: $43,076.92, which annualizes to $80,000 (× 26 ÷ 14).

- Net pay. — take-home after all withholding. Reveals whether the money actually lands; reviewers match it to bank-statement deposits. Caleb: $2,424.34/period, matching his direct deposits.

- Tax withholding. — federal income tax, Social Security at 6.2%, Medicare at 1.45% per the SSA wage base, and state tax. Reveals genuine W-2 employment; a stub claiming a salaried job with no withholding is the most common fabrication tell. Caleb: $652.58 total, including Ohio state tax.

- Employer identity. — legal name, address, phone. Reveals whether the employer can be reached for verification per the FTC's guidance for landlords. Caleb: a Columbus employer with a working HR line.

- Pay-period dates. — period start, end, pay date. Reveals recency (is the stub from the last 30–60 days?) and continuity (no unexplained gaps). Caleb: consecutive biweekly periods through last month.

- Deductions. — pre-tax benefits, and critically, garnishments or child-support orders. Reveals reduced real disposable income; a high gross with a 25% garnishment supports less rent than the headline suggests. Caleb: standard pre-tax only, no garnishment.

- Reconciliation math. — gross minus all deductions and taxes should equal net, every period. Reveals fabrication faster than anything else, because faked stubs rarely tie out to the cent. Caleb: $3,076.92 − $652.58 = $2,424.34 ✓.

- Cross-document consistency. — the stub against the bank statement, the photo ID, and the application. Reveals identity and income mismatches no single document shows. Caleb: name, employer, and net all agree across documents.

The Three Reconciliation Checks That Catch a Fake Stub

Examination boils down to three reconciliations a reviewer runs in under two minutes. If all three tie out, the stub is almost certainly real; if any one fails, it is the line to question.

| Check | What it tests | Caleb's math | Result |

|---|---|---|---|

| Period reconciliation | Gross − taxes − deductions = net | $3,076.92 − $652.58 = | $2,424.34 ✓ |

| YTD annualization | YTD ÷ periods elapsed × periods/year = stated salary | $43,076.92 ÷ 14 × 26 = | $80,000 ✓ |

| Cross-document match | Stub net = recurring bank deposit; names agree | $2,424.34 = direct deposit | Match ✓ |

The single most useful number to examine is net pay, because it is the one figure that has to appear twice — once on the stub, once as a deposit on the bank statement. A fabricated stub can show any gross the author wants, but matching a fake net to real bank deposits across three consecutive periods is hard to fake and easy to check.

Reading the Frequency Before the Number

Data point #2 deserves its own table because frequency errors are the most common honest mistake in examination — counting a weekly stub as biweekly halves the income; counting a biweekly as semi-monthly distorts the YTD check.

| Pay frequency | Periods/year | Annualize gross by | Caleb-scale example |

|---|---|---|---|

| Weekly | 52 | gross × 52 | $1,538.46 → $80,000 |

| Biweekly | 26 | gross × 26 | $3,076.92 → $80,000 |

| Semi-monthly | 24 | gross × 24 | $3,333.33 → $80,000 |

| Monthly | 12 | gross × 12 | $6,666.67 → $80,000 |

Caleb's Stub, Line by Line

The full per-period computation Renée examined, in the order it prints:

| Line | Math | Amount |

|---|---|---|

| Gross | $80,000 ÷ 26 | $3,076.92 |

| Federal income tax | Pub 15-T %-method, single, biweekly | −$340.27 |

| Social Security | 6.2% × $3,076.92 | −$190.77 |

| Medicare | 1.45% × $3,076.92 | −$44.62 |

| Ohio state income tax | Ohio withholding tables, biweekly | −$76.92 |

| Net pay | $3,076.92 − $652.58 | $2,424.34 |

Federal withholding is shown via the IRS Publication 15-T percentage method; Social Security and Medicare are the fixed FICA rates; Ohio tax comes from the state withholding tables. The point of examining the line items is not to recompute payroll — it is to confirm the lines exist and that they sum to the printed net. They do, so Caleb's stub passes the period reconciliation.

Clean Data vs. a Stub That Should Be Questioned

Examining the data is most valuable when it surfaces a problem. The contrast below puts Caleb's clean stub beside the patterns that should trigger a closer look or a verification call.

| Signal examined | Caleb's clean stub | Stub that should be questioned |

|---|---|---|

| Tax withholding | Federal, FICA, and state all present | No withholding on a "W-2" job |

| Net vs. bank deposit | $2,424.34 = the direct deposit | Net has no matching deposit |

| Period math | Gross − deductions = net to the cent | Gross − deductions ≠ net |

| YTD annualization | Annualizes to $80,000 | YTD implies a wildly different salary |

| Round numbers | Taxes are odd cents (real calc) | Every figure is a suspiciously round number |

| Employer | Reachable phone and address | No phone, PO box only, unverifiable |

| Name consistency | Matches ID and application | Nickname or mismatch across documents |

| Pay-period dates | Recent, consecutive | Stale, overlapping, or impossible dates |

| Font/format drift | Consistent throughout | Misaligned columns, mismatched fonts |

Who Reads the Data and What They Want

The same ten data points get examined by different people for different reasons, and the way apartments verify income builds directly on them. Knowing who weighs what tells a renter which numbers to get right.

| Examiner | Primary question | Data points weighted most |

|---|---|---|

| Renter (self-check) | Will my file pass on the first read? | Name match, net vs. deposit, YTD annualization |

| Landlord / property manager | Will rent be paid on time? | Gross vs. 3×, net stability, garnishments |

| Tenant-screening platform | Is this stub real and consistent? | Reconciliation math, employer verification |

| Mortgage lender | Is income durable for years? | YTD, two-year history, W-2 reconciliation |

| Employer / payroll (on a verify call) | Did we issue this? | Employer block, dates, gross, net |

Mistakes Reviewers (and Renters) Make Examining Data

The errors below come from examining the data carelessly — they produce both wrong rejections and missed fabrications:

- Reading gross as net (or vice versa), then misjudging both the 3× ratio and the deposit match

- Ignoring pay frequency, so a biweekly stub gets annualized as monthly or weekly

- Trusting a round number — real withholding produces odd cents; all-round figures are a fabrication tell

- Skipping the bank-statement cross-check, the single best test that net pay is real

- Treating a wage garnishment as irrelevant when it materially cuts disposable income

- Penalizing a mid-year start without asking — a low YTD can simply mean the applicant began in April

- Mistaking state payroll lines for errors — New Jersey's four deductions or California SDI are normal, not red flags

- Examining one stub instead of three, so consistency can't be tested

- Letting a high salary excuse a failed reconciliation — clean math on a modest income beats broken math on a big one

- Making a screening decision on a gut feeling the data does not support, which is both unfair and an FCRA risk

When examination surfaces something that does not reconcile, ask before you decide. Renters can use the same structure pre-emptively to explain a discrepancy. Copy, paste, and fill the brackets.

| Examination check | Caleb's stub passes when |

|---|---|

| Gross monthly income ≥ 3× rent | $6,666.67 ≥ $6,300 needed ✓ |

| Pay frequency identified and applied | Biweekly → × 26 |

| YTD annualizes to the stated salary | $43,076.92 → $80,000 |

| Net pay matches a recurring bank deposit | $2,424.34 = direct deposit |

| Federal, FICA, and state withholding present | All four tax lines shown |

| Employer name, address, and phone verifiable | Columbus employer, HR line works |

| Pay-period dates recent and consecutive | Through last month, no gaps |

| No undisclosed garnishment or support order | None on the stub |

| Period math reconciles (gross − deductions = net) | $3,076.92 − $652.58 = $2,424.34 |

| Stub, ID, and application names agree | "Caleb Monroe" on all three |

| Figures are not suspiciously round | Taxes carry real odd cents |

Examining Data Without Breaking FCRA or Fair Housing

Examining stub data is not just good practice — for a landlord using a screening report, it is part of staying inside the law. The FCRA and the Fair Housing Act set the guardrails.

| Situation | Rule | Source |

|---|---|---|

| Denying based on a screening report | Provide an adverse-action notice naming the company | CFPB |

| Applicant disputes the report's accuracy | The screening company must reinvestigate | FCRA §611 / FTC |

| Examining income | Apply the same standard to every applicant | HUD Fair Housing |

| Rejecting a lawful income source | Source-of-income laws may bar it (varies) | HUD + state/local law |

| Keeping applicant documents | Store and dispose of consumer data securely | FTC Disposal Rule |

The through-line is consistency: examine the same data points by the same standard for every applicant, document the income-based reason for any denial, and honor the adverse-action and dispute process when a report is involved. A reviewer who examines the data the same way every time both makes better decisions and stays defensible. For renters, the mirror rule is to examine your own data first so the reviewer's checks pass without a single follow-up question.

Why do landlords examine pay stub data so closely?

Because the headline salary alone predicts nothing. Examining the data tells a landlord whether the income clears the rent ratio, whether it is real (taxes withheld, employer verifiable), and whether it is stable (year-to-date annualizes, net matches deposits). A stub can show any number; the data underneath is what reveals whether that number is earned and durable. Close examination also protects the landlord legally — a tenant-screening report is governed by the FCRA, so a denial needs a documented, income-based reason, not an impression. The two minutes of examination prevent both bad approvals and unfair, legally risky rejections.

What does examining a pay stub reveal that a credit check doesn't?

A credit check shows how someone has handled past debt; it does not show current income. Examining a pay stub reveals the present run-rate — gross, frequency, and net — plus whether that income is real and stable. The two are complementary: strong credit with no documentable income still cannot pay rent, and high income with a failed reconciliation is a fabrication risk. Examination also surfaces things a credit report never carries: a wage garnishment cutting disposable income, an employer that cannot be verified, or a net pay that has no matching bank deposit. Together they give a fuller picture than either alone.

How can you tell if a pay stub is fake?

Examine three things. First, the math : gross minus taxes and deductions should equal net to the cent, and real withholding produces odd cents rather than suspiciously round numbers. Second, the bank match : the net pay should appear as a recurring deposit on the bank statement across consecutive periods. Third, the annualization : year-to-date divided by periods elapsed, times periods per year, should equal the stated salary. Fabricated stubs usually break on at least one of these, plus tells like missing tax withholding, an unverifiable employer, formatting drift, or impossible pay-period dates. A verification call to the employer settles anything the math leaves ambiguous.

Why does year-to-date matter when examining a stub?

Year-to-date is the stability check. A single period shows a snapshot; YTD shows the trajectory and lets a reviewer confirm the income is continuous and annualizes to the salary claimed. Divide YTD by the number of periods elapsed and multiply by periods per year — the result should match the stated annual income. A YTD that implies a very different salary signals a recent raise, a mid-year start, a bonus, or a fabrication, and each deserves a question. For Caleb, YTD of $43,076.92 at period 14 annualizes cleanly to $80,000, which is why the figure passes examination without a follow-up.

Should I examine my own pay stub before I apply?

Yes — it is the single best way to avoid a slow or denied application. Run the same checks a reviewer will: confirm your name matches your ID exactly, that gross monthly income clears 3× the rent, that year-to-date annualizes to your salary, that net pay matches your bank deposits, and that all tax lines are present. Catching a nickname, a mismatched deposit account, or an unexplained mid-year YTD while you can still attach a short note or a corrected stub keeps the reviewer from having to ask. A self-examined packet passes on the first read, which in a competitive market is often what wins the unit.

Does a wage garnishment on my stub hurt my application?

It can, because a garnishment reduces the disposable income available for rent, and an examining reviewer will notice it. A garnishment does not automatically disqualify you, but it lowers the effective income behind the 3× rule, so a stub with a high gross and a large garnishment may support less rent than the headline suggests. If you have one, get ahead of it: document the income that remains after the garnishment, add a co-signer or extra deposit if the post-garnishment ratio is tight, and explain the situation briefly rather than letting the reviewer discover it. Transparency reads better than a surprise.

What does it mean if a stub has no taxes withheld?

On a stub that claims W-2 employment, missing federal, Social Security, and Medicare withholding is a major red flag and one of the most common signs of a fabricated stub. Legitimate W-2 wages always carry FICA at 6.2% and 1.45%, plus federal and usually state income tax. The honest exceptions are genuine independent contractors, who receive a 1099 and no withheld stub at all, and certain very-low-earnings periods — but those should be labeled as contractor income, not presented as W-2 wages. If a stub claims salaried employment with zero withholding, examine the rest of the document closely and verify with the employer before relying on it.

Can examining stub data violate fair housing or FCRA rules?

Examining the data itself is fine and expected — the rules govern how you apply it. Under the Fair Housing Act, you must examine every applicant by the same standard and never let a protected class drive the decision. Under the FCRA, if a tenant-screening report contributes to a denial, you must provide an adverse-action notice naming the screening company, and the applicant can dispute inaccuracies. The compliant pattern is consistency and documentation: examine the same data points the same way for everyone, base any denial on a documented income reason, and honor the notice-and-dispute process. Done that way, examination strengthens a decision rather than exposing it. — Lena Brooks, Rental & Tenant-Screening writer at MyStubs. Lena covers rental applications, income verification, and the FCRA rules that govern tenant screening, with a focus on what leasing offices and screening platforms actually examine before they approve a file.

Official sources

Sources · 11 references

- U.S. Department of Labor — FLSA Recordkeeping Fact Sheet 21

- Federal Trade Commission — Tenant Background Checks

- Federal Trade Commission — Using Consumer Reports: What Landlords Need to Know

- Federal Trade Commission — Fair Credit Reporting Act (full text)

- Consumer Financial Protection Bureau — Notice of Adverse Action

- U.S. Department of Housing and Urban Development — Fair Housing Act Overview

- Internal Revenue Service — About Form W-2

- Internal Revenue Service — About Form 1099-NEC

- Internal Revenue Service — Publication 15-T, Federal Income Tax Withholding Methods

- Social Security Administration — 2026 Contribution and Benefit Base

- Ohio Department of Taxation — Employer Withholding Tables

Discussion

No comments yet — be the first to share a state-specific note, a follow-up question, or a correction.